Asset Planning and Protection Business is tough, there are many challenges and sometimes unexpected events can occur. Hundreds of businesses fail each year and often this can leave the business owner seriously distressed emotionally and financially.

Business is tough, there are many challenges and sometimes unexpected events can occur. Hundreds of businesses fail each year and often this can leave the business owner seriously distressed emotionally and financially.

However, with some prior planning it can be possible to reduce some of the risks faced by business owners. This item considers some of the risks that business owners face and legitimate means to reduce those risks.

CONSIDER THE FOLLOWING EXAMPLE

A YEAR AGO

George has been operating his own electrician business for 4 years which he set up after working for several years for a large electrical company. On the advice of a friend he established a company, “George’s Electrical Ltd,” (GEL for short) to be the vehicle through which the business is carried on. George owns all the shares in GEL. He was told that this would give him limited liability and for extra protection GEL has taken out a public liability insurance policy. George owns his own home which he partly financed with a mortgage from ABC Bank Ltd. His girlfriend has been living with him for 3 years.

Business has been good and GEL employs three other electricians and a part-time office assistant. GPL builds up a good history with several electrical supply companies and is granted extended credit terms. One of the electrical supply companies asked George to sign a personal guarantee which he did. GEL has a bank overdraft with ABC Bank Ltd which also had George sign a personal guarantee. George is enjoying a good lifestyle with an overseas trip every year and a nice car and boat.

GEL has a successful property developer client, “Harry,” who is building several large blocks of apartments in the name of Flash Harry Developments Ltd. GEL is providing all the plumbing materials required. It is a big contract for GEL but very profitable.

FIVE MONTHS LATER

Initially Harry was paying GEL’s bills regularly but has now fallen several months behind. This is causing some stress for George as GEL’s bank overdraft is now at its limit and GEL has got behind in paying its suppliers. GEL has also not paid PAYE and GST to Inland Revenue for the last two months. George is wondering if he should stop supplying Harry until the bills are paid up to date. When George raises this with Harry at one of Harry’s extravagant parties, he is told don’t worry extra money is coming soon from new financiers in Dubai. Harry promises an extra bonus if George’s company stays on the job and gets the work finished on time.

A FURTHER MONTH LATER

George is on holiday in Fiji with his girlfriend and receives a call from one of GEL’s employees saying that they turned up at one of the apartment blocks to find that Harry’s bankers, XYZ Bank Ltd, have appointed a receiver and are preventing contractors from entering the site. George cuts his holiday short and returns to NZ on the next available flight to find that all of Harry’s apartment buildings are in the hands of the receiver. He argues with the receiver that he should be able to remove the materials his company has provided but the receiver says no, the XYZ Bank has a GSA (whatever that means) and the materials will be sold with the proceeds paid to the Bank.

A FURTHER TWO MONTHS LATER

GEL is now finding it difficult to pay any bills and is overdue paying staff wages. Two of the employees have stopped working and are ringing him constantly demanding payment of their overdue wages. Inland Revenue is also chasing him over the unpaid GST and PAYE and to top it all off his girlfriend leaves him and moves in with Harry who is still driving an Aston Martin and living a lavish lifestyle.

George then receives a letter from the ex-girlfriend’s lawyer claiming a half share in the house and all his other assets including the business.

He also receives a notice from ABC Bank that they require him to personally repay GEL’s overdraft or else they will sell his home in a mortgage sale.

A FURTHER FOUR MONTHS LATER

George has been evicted from his home, which has been sold in a mortgagee sale by the ABC Bank to repay GEL’s overdraft. His ex-girlfriend has been awarded his car and boat. He has been declared bankrupt and had to move in with his mum and go on the dole.

He is being prosecuted by Inland Revenue which had GEL placed into liquidation and the business closed down.

He is also facing assault charges for punching Harry when he saw him with the ex-girlfriend outside an expensive restaurant.

George now finds the best way to deal with his problems is to go to the pub every afternoon and stay there until he staggers home at closing time.

AN EXTREME EXAMPLE? NO, THIS STORY IS NOT UNCOMMON BUT WHAT COULD HAVE BEEN DONE BETTER?

CONTRACT WITH FLASH HARRY DEVELOPMENTS LTD

GEL’s terms of trade should have included a Romalpa clause which effectively states that GEL retains ownership of all materials provided and has a right of entry to reclaim them until they are paid for in full. For significant contracts, such as with Flash Harry Developments Ltd, GEL should have registered a Purchase Money Security Interest (PMSI) on the Personal Property Securities Register (PPSR). If done correctly the PMSI would have given GEL priority over the XYZ Bank’s General Security Interest (GSA).

At the time of entering into the contract PML could have requested a personal guarantee from Harry and some security such as a bond or letter of credit. Although this might have been denied it is worth considering. Contractors should also ensure that their invoices refer to the Construction Contracts Act where applicable. This will not give any priority but can help if amounts are later disputed. When Harry got behind on the bills, George might have been better to cut his losses and quit the project then. Contractors will always have to balance commercial considerations but generally the biggest losses arise when original credit terms are departed from.

OWNERSHIP OF GEL

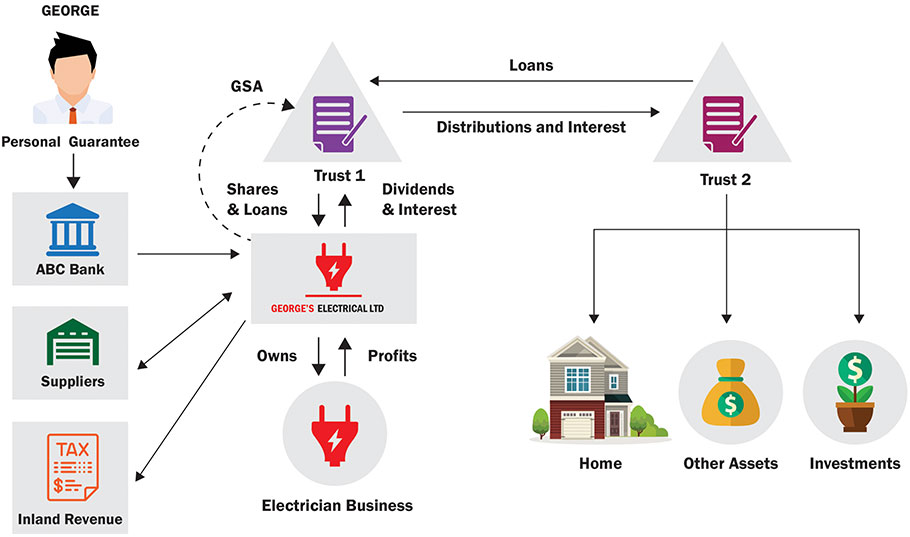

George could have established a Trust to own the shares in GEL. An independent trustee could have been appointed as a trustee of the Trust. A trust as shareholder could have allowed surplus profits to be taken out of GEL by way of dividend. Generally, dividends could have been paid out if GEL would still be solvent after paying the dividends and the terms of any bank covenants allowed payment of dividends. The Trust might need to lend some of the dividends received back to GEL in which case GEL could pay interest to the Trust and the Trust take a GSA. This could give the Trust priority over other creditors of GEL, the main exceptions being any creditor with a prior ranking GSA such as ABC Bank, Inland Revenue in respect of PAYE, unpaid wages, and any creditor who has a PMSI properly registered. Despite these exceptions, many creditors will be unsecured. A Trust might also offer some tax advantages in certain circumstances.

OWNERSHIP OF HOUSE AND OTHER ASSETS

George should have had his home and other significant assets owned by a Trust. This could be the same Trust to own the shares in GEL but even better if it is a separate Trust with some difference in trustees. A separate Trust could help avoid the house being drawn into any claim against the shareholder of GEL, for example, if the shareholding Trust guaranteed any company debts or there is a claim for return of any dividend. The shareholding Trust could possibly make beneficiary distributions to the home owning Trust thereby further isolating wealth from business risk.

Also, if possible it would be better that mortgage finance is from a different bank than the bank financing the business. This would further protect the house from creditors of the business. If this is not possible, George could have asked ABC Bank to exclude the home from being used to secure the business debt or for the exposure to be limited to some extent.

Ownership of the house and other assets by a Trust could also have helped to resist the claim from George’s girlfriend since George wouldn’t personally be the owner of the house. There are no guarantees though as this is a continually evolving area of the law. There have been some cases where relationship claimants have manged to access assets held in trusts. However, it is clear in many circumstances that a relationship claim is far more likely to be upheld when assets are owned personally than when held in a Trust.

PERSONAL GUARANTEES

These can be hard to avoid but should be resisted wherever possible. Generally, banks won’t lend to small businesses without a personal guarantee but suppliers who request personal guarantees might still provide some credit if the director or the shareholder of the company declines to give a personal guarantee. A point to note with guarantees is that once given, care must be taken with any subsequent transfer of assets to a Trust. If not managed correctly the assets transferred to the Trust could still be subject to the personal guarantee.

INLAND REVENUE

George should have ensured that PAYE and GST debts were paid in priority to other amounts. In particular PAYE belongs to the Crown from the outset and non payment of it can cause company directors to be prosecuted. Inland Revenue is quite aggressive when it comes to recovering PAYE.

CASHFLOW PLANNING

Proper budgeting and monthly monitoring can help anticipate cashflow problems before they occur thereby allowing an opportunity to take corrective action where possible. In some cases it can be prudent for monthly financial accounts to be prepared promptly after each month end with a comparison to budgeted results. These may also assist with arranging additional finance to smooth over temporary cashflow problems.

INSURANCE

Although not relevant to the above example, careful consideration should be given to both business and personal insurance. Business owners should ensure that they personally have adequate cover for life, health, income protection and trauma, and that this is regularly reviewed and updated.

EXAMPLE OF POSSIBLE STRUCTURE

The above is of a general illustrative nature only and should not be relied upon as advice in any particular circumstances. Specific professional advice should be obtained in every case